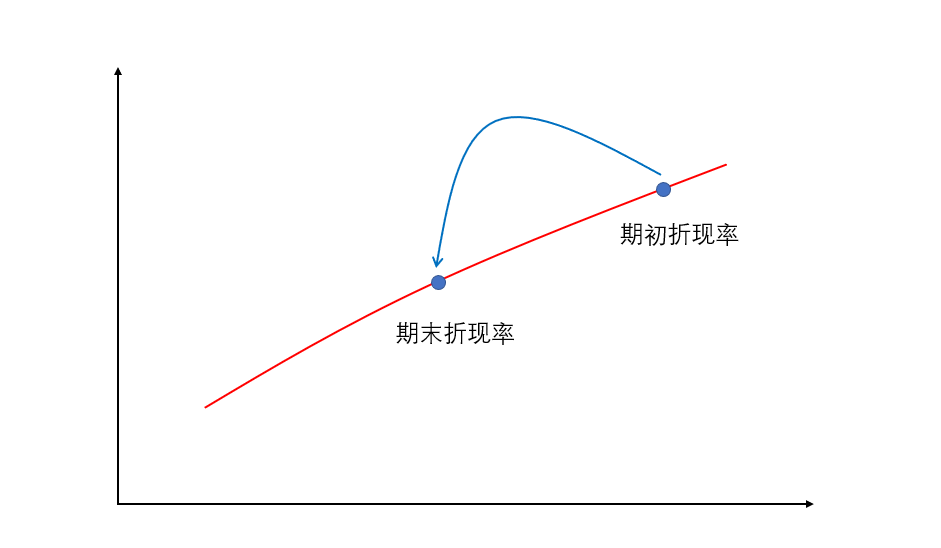

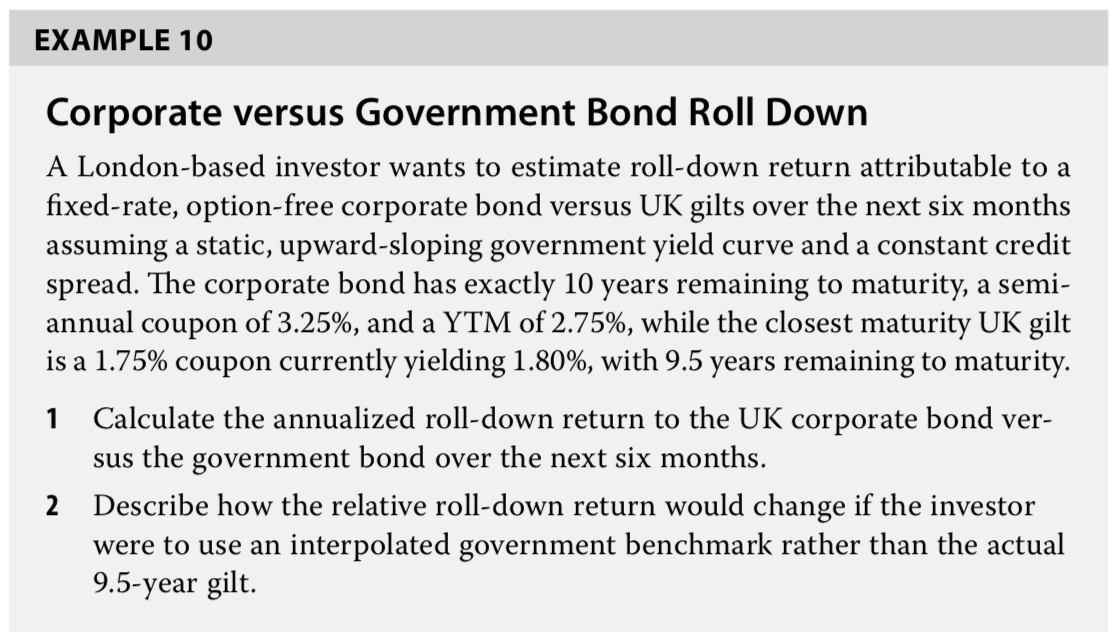

老师能不能解释一下第二问答案中后面这句话怎么理解?非常感谢!Solution to 2: The interpolated benchmark involves the use of the most liquid, on-the-run government bonds to derive a hypothetical 10-year UK gilt YTM. Because the UK gilt yield curve is upward sloping in this example, we can conclude that the relative roll-down return using an interpolated benchmark would be lower than the 0.95% difference in Question 1.