NO.PZ201809170400000604

问题如下:

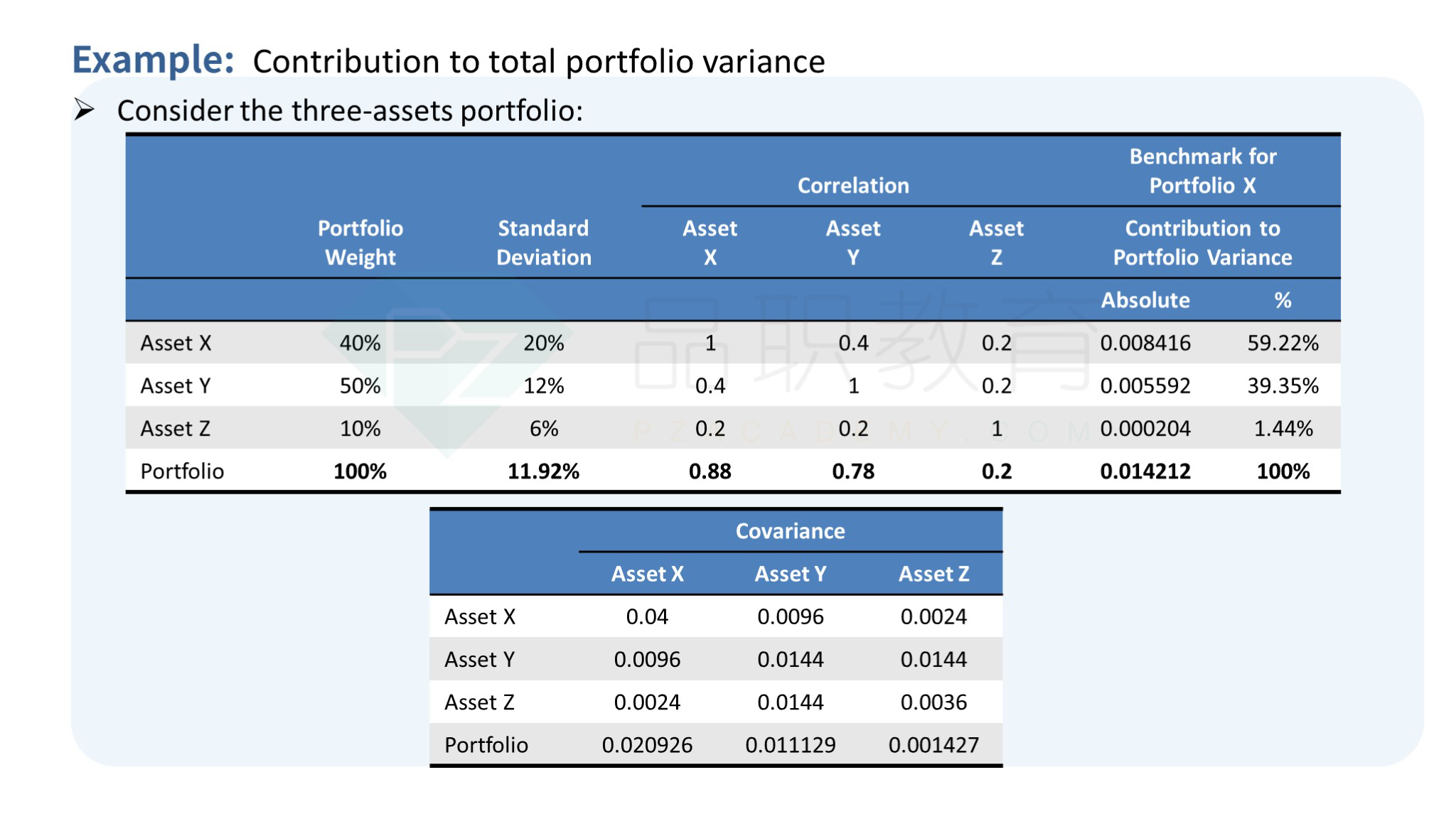

Based on Exhibit 1, the contribution of Asset 2 to Manager C’s portfolio variance is closest to:

选项:

A.0.0025.

B.0.0056.

C.0.0088.

解释:

B is correct. The contribution of an asset to total portfolio variance equals the summation of the multiplication between the weight of the asset whose contribution is being measured, the weight of each asset (xj), and the covariance between the asset being measured and each asset (Cij), as follows:

Contribution of each asset to portfolio variance = CVi

The contribution of Asset 2 to portfolio variance is computed as the sum of the following products:

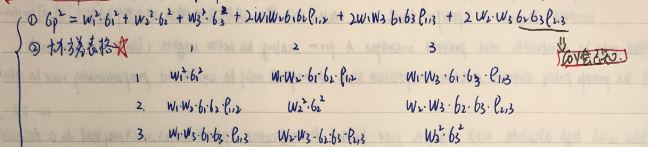

分母应该怎么算?列一个3*3的表格然后把所有框里的相加吗