NO.PZ2021101401000010

问题如下:

Yuen and Ruckey design a Benchmark Portfolio (A) and a Risk Parity Portfolio (B), and then run two simulation methods (the historical simulation and Monte Carlo simulation) to generate investment performance data based on the underlying nine factor portfolios.

Yuen and Ruckey discuss the differences between the two simulation methods. During the process, Yuen expresses a number of concerns:

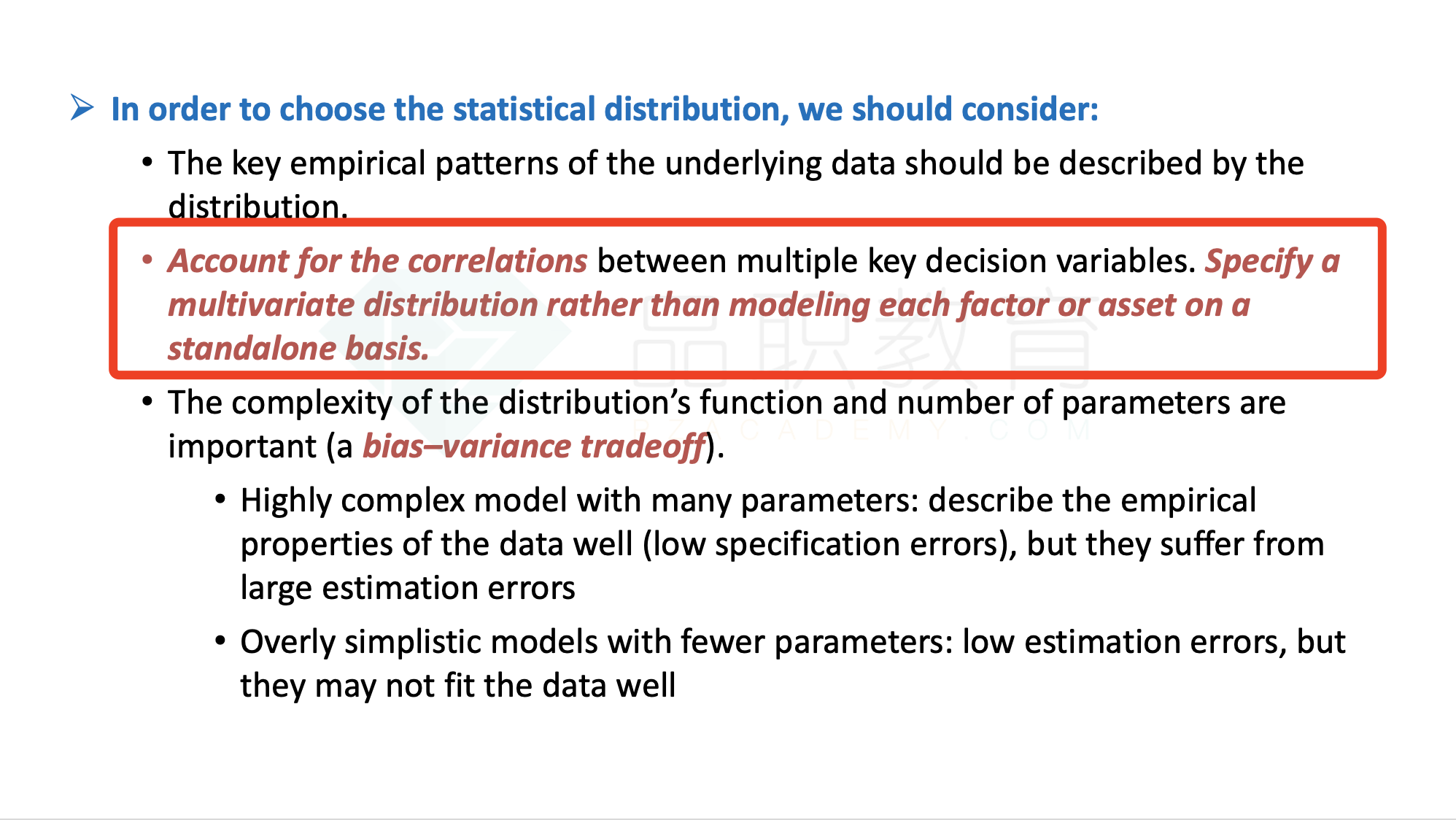

• Concern 1: Returns from six of the nine factors are correlated.

To address Concern 1 when designing Monte Carlo simulation, Yuen should:

选项:

A.

model each factor or asset on a standalone basis.

B.

calculate the 15 covariance matrix elements needed to calibrate the model.

C.

specify a multivariate distribution rather than modeling each factor or asset on a standalone basis.

解释:

C is correct. Under Monte Carlo simulation, the returns of Portfolios A and B are driven by the returns of the nine underlying factor portfolios (based on nine common growth factors). In the case of asset or factor allocation strategies, the returns from six of the nine factors are correlated, and therefore it is necessary to specify a multivariate distribution rather than modeling each factor or asset on a standalone basis.

A is incorrect. The returns of six of the nine factors are correlated, which means specifying a multivariate distribution rather than modeling each factor or asset on a standalone basis.

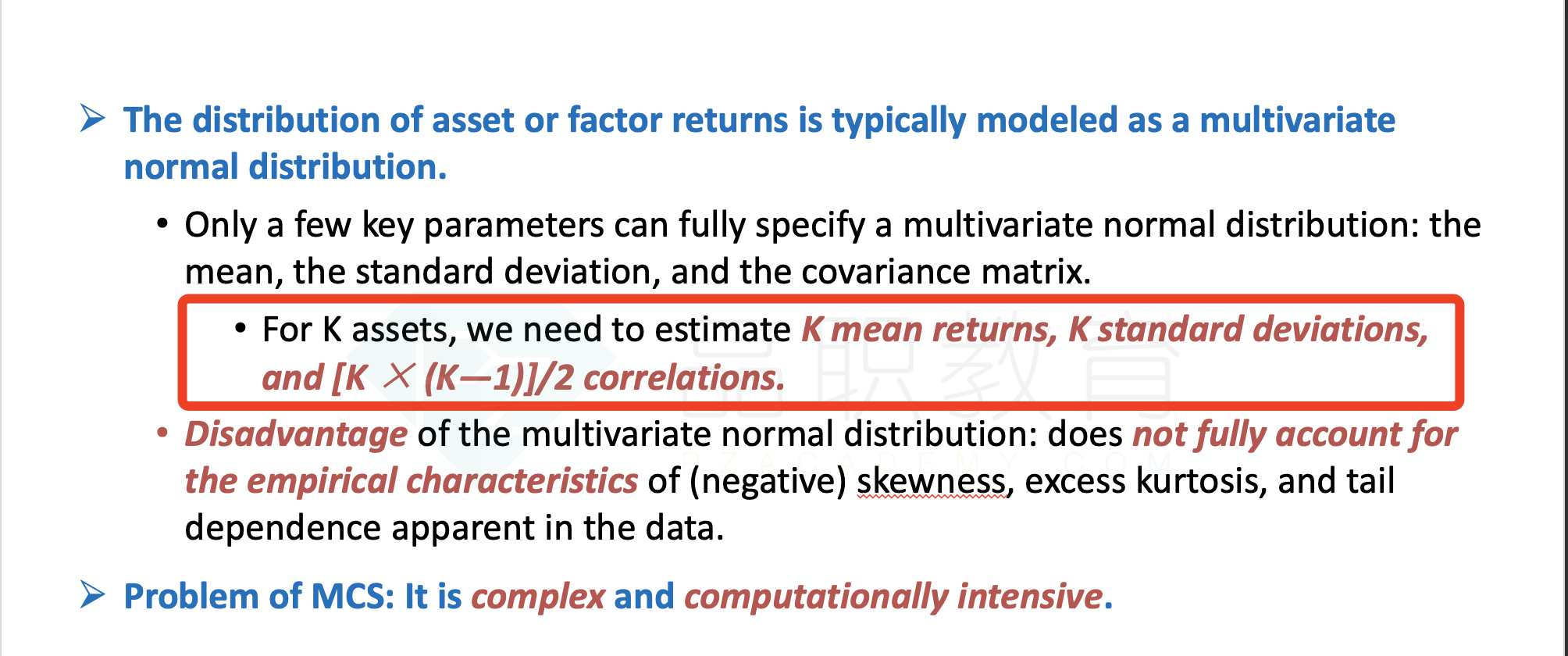

B is incorrect because the analyst should calculate the elements of the covariance matrix for all factors, not only the correlated factors. Doing so entails calculating 36, not 15, elements of the covariance matrix. Monte Carlo simulation uses the factor allocation strategies for Portfolios A and B for the nine factor portfolios, the returns of which are correlated, which means specifying a multivariate distribution. To calibrate the model, a few key parameters need to be calculated: the mean, the standard deviation, and the covariance matrix. For 9 assets, we need to estimate 9 mean returns, 9 standard deviations, and the elements of the covariance matrix is

Assuming just the 6 correlated assets, the calculation is

这是哪一个小章节的内容