NO.PZ201601050100001704

问题如下:

The derivative product first suggested by Regan as a potential hedge strategy for

Portfolio B:

选项:

A.

is a relatively liquid contract.

B.

eliminates counterparty credit risk.

C.

allows Monatize to keep voting rights on its equity portfolio.

解释:

C is correct.

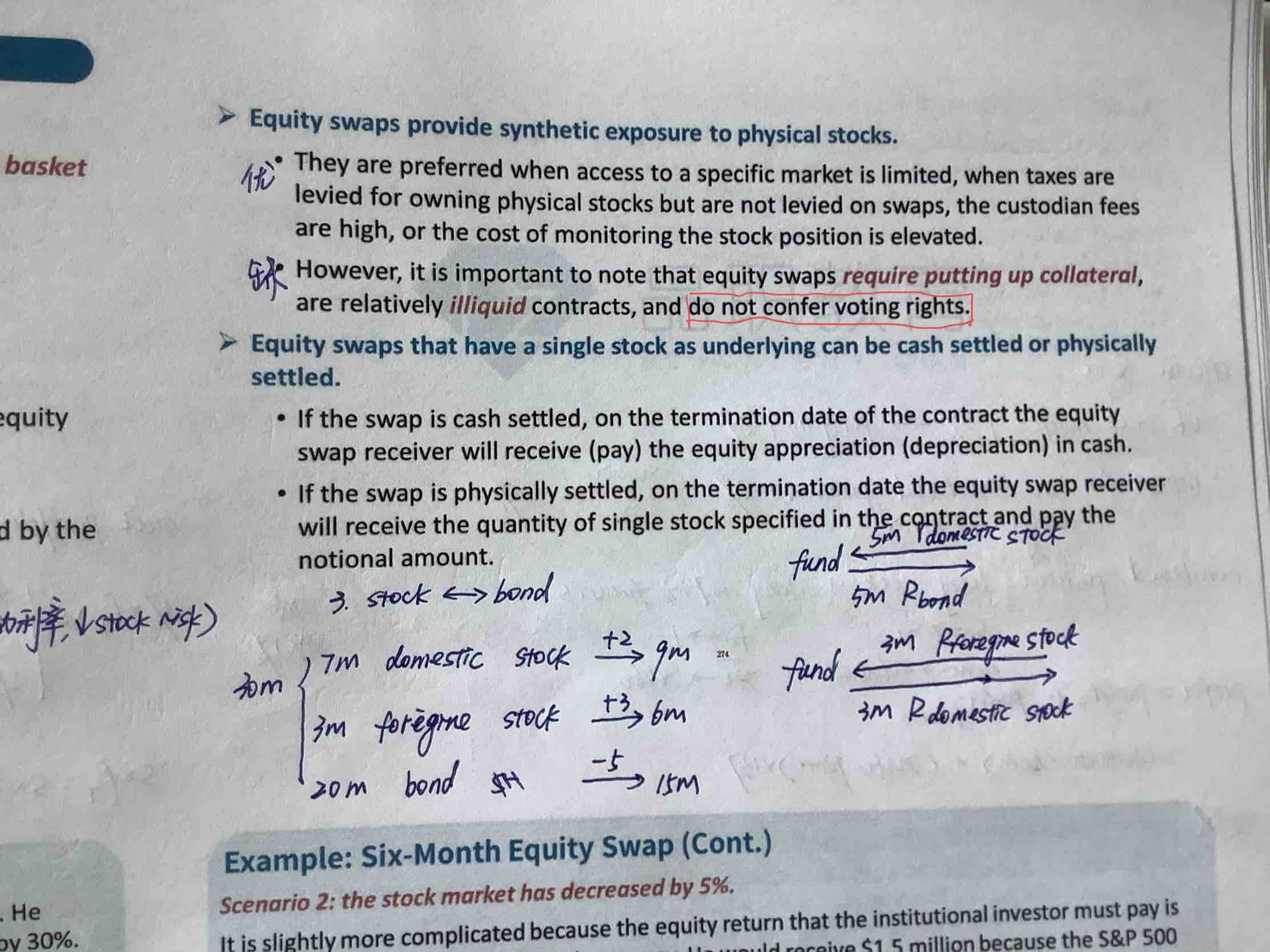

The first hedging strategy suggested by Regan is entering into a

total return equity swap in exchange for a fee. Equity swaps, which are relatively illiquid contracts and are OTC derivative instruments in which each party

bears counterparty risk, do not confer voting rights to the counterparty receiving the performance of the underlying. Under the terms of the total return

equity swap, at pre-specified dates, the counterparties will net the index total

return (increase/decrease plus dividends) against the fixed interest payment.

If the index total return exceeds the fixed interest payment, Monatize will pay

the counterparty the net payment. If the index total return is less than the

fixed interest payment, then Monatize will receive the net payment from the

counterparty.

A is incorrect because equity swaps are relatively illiquid contracts.

B is incorrect because equity swaps are OTC derivative instruments, and each

counterparty in the equity swap bears the risk exposure to the other counterparty. For this reason, equity swaps are usually collateralized in order to reduce

credit risk exposure.

中文解析:

本题考察的是equity swap。

Equity swap是OTC的衍生工具,流动性相对较差,交易双方都承担交易对手风险。A.B选项错误。

Total return equity swap指的是合约的一方会将股票相关的所有的return都付给对手方,既包括股价增值的部分又包括分发的股利。但是股票并没有给到对手方,因此投票权还保留,所以C选项正确。

讲义上不是说不保留投票权吗