NO.PZ201712110200000401

问题如下:

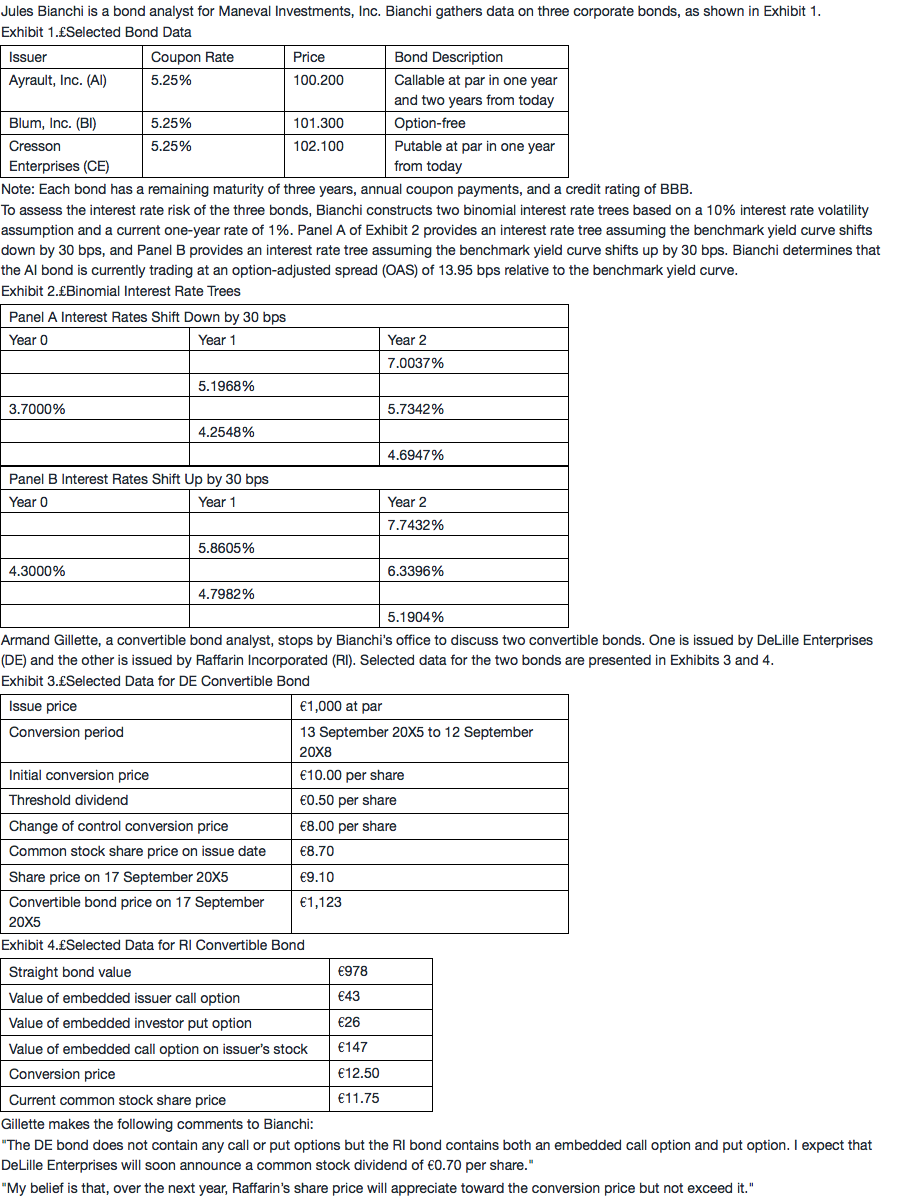

Based on Exhibits 1 and 2, the effective duration for the AI bond is closest to:

选项:

A.1.98.

B.2.15.

C.2.73.

解释:

B is correct.

The AI bond’s value if interest rates shift down by 30 bps (PV–) is 100.78. The AI bond’s value if interest rates shift up by 30 bps (PV+) is 99.487.

Effective duration=[(PV-)-(PV+)]/[2× (ΔCurve) × (PV0)]= (100.780 - 99.487)/ (2 × 0.003 × 100.200)=2.15

[0.5*(100+100)+5.25]/1.071432=98.23

[0.5*(100+100)+5.25]/1.058737=99.41

[0.5*(100+100)+4.8342]/1.048342=100

[0.5*(98.23+99.41)+5.25]/1.053363=98.80

[0.5*(99.41+100)+4.3943]/1.043943=99.71

PV0=[0.5*(98.80+99.71)+3.8395]/1.038395=99.28